Metromile: InsurTech & SPAC Dreams

After beginning a twitter thread which was getting too long here I am on substack. Whether I will ever write another one of these, I don’t know. But I wanted to share my thoughts on this one and comment on SPACs more broadly. I am going to assume a certain level of knowledge in this write-up so if you don’t know what a SPAC is, you’re not the target audience. For those who do, I hope you enjoy reading it…as much as I enjoyed writing it.

Please remember that nothing I have written here is investment advice and if you need investment advice you should not be investing in individual companies.

Today we will be looking at Insurance Acquisition Corp II ($INAQ), one of the latest SPACs to announce an InsureTech deal to bring Metromile public. In terms of background $INAQ is a SPAC that is sponsored by Cohen & Co. ($COHN) a small broker-dealer / asset manager which itself has a colorful history.

Cohen & the Current SPAC Landscape

“A blank-check company by any other name would smell just the same.” - William Shakespeare

Sunset Financial was a mortgage REIT that listed on the stock market in late 2004. In 2006, Sunset announced a reverse merger with privately held Alesco Financial Trust.

Some shareholders were not too happy about the transaction which is not all that surprising given the fact that they were going to be trapped in this new entity at a diminution of value as can be seen in the presentation here. Stories about said shareholder sadness can be found here and here.

The newly named Alesco Financial Inc. (just like the former Alesco Financial Trust) was to pay a 1.5% management fee along with an incentive fee to its manager (Cohen & Co.) for the management of CDOs, CLOs, and similar securitized obligations which were invested mainly in mortgage loans, Trust Preferred Securities (or TruPS), and leveraged loans. Even if you don’t know what some of these terms mean, you vaguely remember CNBC attempting to explain these to you after the financial crisis.

And so we fast-forward to 2009 when Alesco’s stock has fallen by over 95% and we get our second reverse merger which brings Cohen & Co. (the manager of Alesco) public along with a 10-for-1 reverse-stock split. Here is the initial presentation on the rational for the merger. According to this presentation Cohen & Co. had AUM of $22.6B back in 2009. As of 9/30/20 that AUM has fallen to $2.65B. Not surprisingly, despite the fact that most stocks bottomed out in 2009 and have recovered nicely, $COHN actually went on to set new lows in 2019, a decade later, having lost another 90+% of it value from the 2009 lows.

Daniel Cohen was and still is the Chairman of Cohen & Co. along with The Bankcorp, Inc. ($TBBK), a bank which was run by his mother Betsy Cohen for many years. According to this article, she resigned in 2014 when the bank was laboring under a consent order related to money laundering compliance. I should add that $TBBK is a bank that trades at roughly the same price it IPO’d at back in 2004, despite having never paid a dividend to its shareholders. For those looking for a little more background on the always interesting Cohen family which has been involved in quite a few public companies over the years you can look here and here.

I went through this analysis not to discredit Metromile as a company (after all they’re just looking for a way to go public), but to instead provide a level of insight into what kinds of companies have been able to sponsor SPACs in the current environment. This is actually Cohen’s second SPAC focused on InsureTech, the first having spawned Shift Technologies ($SFT). The Cohens also sponsored FinTech Acquisition Corp I, II, III, & IV and a registration statement for FinTech Acquisition Corp V is already filed. It seems the opportunities to deploy capital intelligently are quite abundant today, despite what you may have heard.

Metromile: The Data Science Company

Here is a link to the press release announcing the acquisition of Metromile. As you can see, Metromile bills itself as “the leading digital insurance platform and pay-per-mile auto insurer”. What exactly qualifies this company to call itself “the leading digital insurance platform” I cannot say, but it does sell pay-per-mile auto insurance which will be my focus here. Below are some additional quotes taken from the press release along with the transcript of a prerecorded call with Daniel Cohen (Chairman of both $COHN and $INAQ), Dave Friedberg (Founder and Executive Chairman of Metromile) and Dan Preston (CEO of Metromile):

Metromile is revolutionizing the fragmented $250+ billion U.S. personal auto insurance market with real-time digital auto insurance personalized for low-mileage drivers.

Our data science-driven technology platform creates a significant advantage, and customers are thrilled with their savings and experience.

We are the largest data science company focused solely on auto insurance.

Our tremendous data advantage – we’ve already collected approximately 3 billion miles of data – has allowed us to build a better auto insurance company from the ground up, with digital technology at its core.

One-third of drivers drive most of the miles and get into most of the accidents. And yet, they might pay the same, fixed rates as the two-thirds of drivers who drive less than half the miles.

When you think about U.S. auto insurance incumbents, they are, at best, marketing companies that deliver an inequitable product to the majority of their customers.

These competitors are unprepared for a changing and increasingly digital world. Their advantage today lies in the scale of human capital and marketing tactics, but the advantage required to compete effectively in modern times lies in being a great technology company.

Now I did pick a lot of these out because of the sheer hyperbole involved in the statements, but I also want to highlight an inconsistency in the underlying message. Mileage-based pricing absolutely works and we know that because UBI (usage-based insurance) has been around for some time in both the consumer and commercial markets.

But the problem is that Metromile is selling itself as a data-science company while still borrowing Progressive’s data (much like Root Insurance did) when designing its rates. For those who have not spent much time in insurance, state rate filings are public and so when a company starts out they tend to copy another company’s rates, having no data of their own. For some reason most of these companies seem to borrow Progressive’s data over others (I’ll let you speculate). Eventually you are supposed to use your own data to set rates. Metromile has even received some pushback from state regulators in California for not using their own data:

So is this a data-science company harnessing the power of telematics to set fair rates based on actual driving or a regular insurance company trying to siphon off a customer segment that drives less than the average? Look no further than the risk section of the registration statement:

Due to Proposition 103 in California, we are currently limited in our ability to use telematics data beyond miles-driven to underwrite insurance, including data on how the car is driven.

California makes up about 58% of premiums written in both 2019 and the first half of 2020. Why would you even enter this market if you’re planning to harness the power of telematics to set insurance rates? Because places like San Francisco have plenty of car owners that use their cars very little. Despite all of the hyperbole about Metromile’s competitors being nothing more than marketing companies what Metromile is doing is targeting a specific segment of the market that would benefit from UBI.

Metromile Results

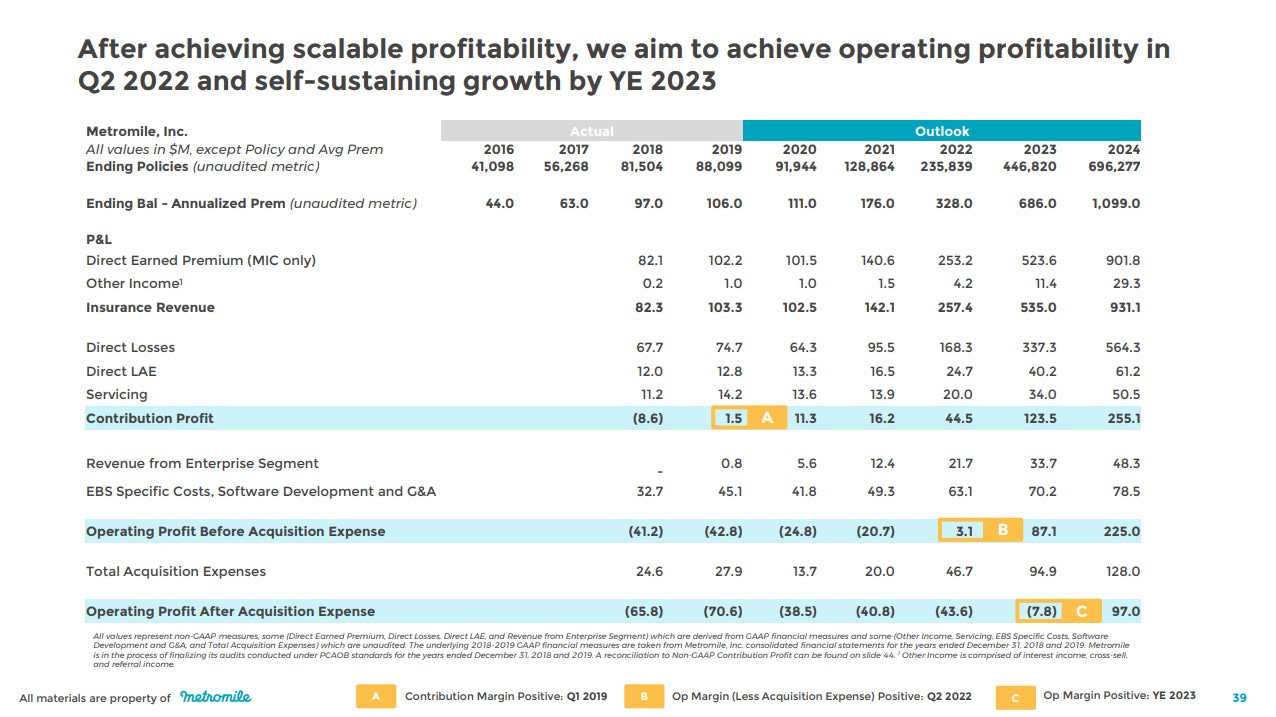

To date it looks like Metromile has raised roughly $310mm of equity and has about $46mm of debt. According to the company’s acquisition presentation at the end of the year it will have annualized direct premiums of $111mm. So it has taken over $3 of capital to produce $1 of annualized premiums, not exactly capital-efficient.

I want to focus your attention on the historical premium growth. Metromile shows a 2016 ending balance of $44mm in annualized premiums. However the annual insurance filing for 2017 shows that they wrote under $5mm in premium in 2016, which means this business really started at the very tail end of 2016 with a very fast initial ramp that quickly burned out. Using their annualized premium numbers from above, for the three years to YE’20 the annualized premium growth rate was just under 21% but if you look at the past two years, that growth rate falls to 7%. Progressive’s growth rate was a whole lot better. If you are wondering why Metromile has barely grown policies of late I direct you to this article.

I pay almost no attention to projections but since these are so curious I will make a few comments. Metromile is forecasting that growth will accelerate from an annualized 7% (over the past two years) to an annualized 77% over the next four years. Here is a funny one…if you divide the annualized year-end premiums by the number of year-end policies you can see that Metromile is projecting average premiums to rise from $1,207 to $1,578 per annum in 2024. This despite the fact that most of their business today is in one of the highest-cost states for auto insurance. In fact, while Metromile has claimed that they are saving their average customer 47% on car insurance their average annual premium is remarkably similar to the 2019 national average of $1,221. So either you think these saving are not real or their current policies are in geographies and customer segments where the cost of insurance is much higher than the national average.

What are the odds that this organization can scale up revenue 10x? What are the odds that they can do this while moving from underwriting in just eight states to underwriting the entire country without even doubling their overhead? You would think this wasn’t a highly regulated industry at the state-level requiring additional overhead for each state - maybe the regulators will streamline their process by using Metromile’s “digital insurance platform”.

Now, lets move on to customer acquisitions costs (CAC) because this requires another leap of faith. Metromile was kind enough to provide the average life expectancy on policies for both new customers and well-seasoned customers (read: over a year old). A new customer policy has an expected life of 3.4 years implying a 2.45% monthly churn (1 / ( 3.4 years x 12 months); a well-seasoned customer policy has an expected life of 5.2 years implying a 1.60% monthly churn. Let’s now assume that the customer mix is fairly well-seasoned because growth has been muted of late - let’s say 65% of customers had a policy in place for over a year by YE’19. The blended monthly churn works out to 1.90% and Metromile would have to replace over 20k policies in 2020. It also expects to have added about 4k new policies by YE’20. Given the $13.7mm acquisition cost provided for 2020 that works out to about $570 per new policy, which is actually a drastic improvement from the 2019 numbers which using 60/40 vs 65/35 split of seasoned vs new policies worked out to >$1,000 per new policy.

Take a moment to think through exactly what kind of margins Metromile would need to justify spending $570 per new policy while generating an attractive return. Using a 2.45% constant monthly churn you need a 20% pre-CAC underwriting margins (an 80 pre-CAC combined ratio) just to make a 10% return despite the fact that the only companies that are close to this are over 30x the size Metromile hopes to be in 2024.

By 2024 the current book of business will be nowhere near as well-seasoned with most customers having recently joined. And so if we assume that half of customer are new (less than a year old) at YE’23 you end up with an expected monthly churn of just over 2%, which means that in 2024 Metromile will need to replace about 140k policies in addition to the roughly 250k policies it hopes to add in 2024. The company has projected they can do this with a mere $128mm in acquisition costs. So what they are saying is that CAC is going to fall from about $570 per policy in 2020 to about $330 per policy in 2024. Great! How?

The OEMs & CAC

Honestly, this is the only upside I see for Metromile and is legitimately a good idea. The idea is that you buy a car and since the OEMs already knows how much you drive (telematics) they can send these low-mileage driver leads to Metromile which can then use the leads to better target their marketing spend rather than say blanketing social media to acquire customers.

Metromile has already signed a deal with Ford to make this possible and I would not be shocked if this was the key to consummation of the SPAC deal. Could this work? Sure. It’s certainly not guaranteed. Just because one person in a family is a low-mileage driver, doesn’t mean the whole family can save money or that the person you are targeting even makes the purchase decision. Still, it’s a good experiment.

Will this provide any kind of lasting competitive advantage to Metromile? Not likely, because insurance is a highly competitive product and if a marketing channel works these leads will likely be bid up, just as happens with search ads. There is actually a pretty good argument for not going public on the possibility that this does work because all you are doing by going public is announcing your strategy to your competitors and showing them the results.

Now the one area that I can’t quite explain is that Metromile claims CAC of $238 in Q2’20 and $289 in Q3’20. They do not provide any data to support that assertion and given the data they have disclosed I can’t come up with a way to verify that. Obviously this is one of the most important numbers in trying to analyze this company, but at this point it’s an act of faith. My guess is that by gutting the marketing department recently they were left with limited but much lower-CAC customer opportunities, but to create the kind of growth they are forecasting they will need to target much higher CAC opportunities. That being said should the OEM channel prove highly efficient I could very well be wrong about that. For those looking to monitor Metromile this is the most important piece of the puzzle.

Is Metromile a Non-Standard Auto Insurer?

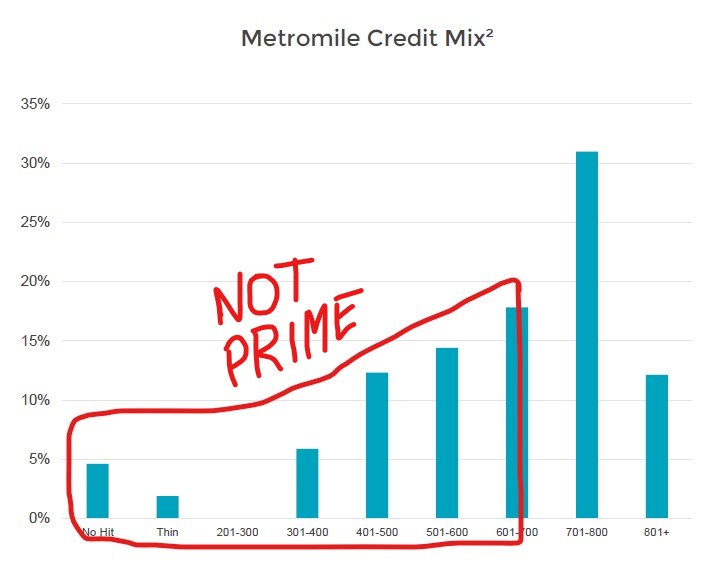

Non-standard auto insurance is broadly grouped in to two categories: poor driving record and poor credits. I was a little puzzled to see Metromile report their credit statistics in their presentation. I would have probably left this page out of the marketing document.

While opinions differ on the exact cutoff, everyone agrees that below 600 credits are subprime, and above 700 are prime. So just eyeballing this you get the sense that about 1/3 of Metromile’s book of business is subprime (excluding customers with thin or no credit and the 600-700 range which include a mix of creditors).

How does that affect insurance in a normal cycle? When people have jobs they generally pay their insurance and when they lose their jobs a lot of them stop paying their insurance. Each state has their own rules about what that means for insurance companies, but just because you missed a payment doesn’t mean you are no longer covered. You will have some amount of time to make the payment before your coverage lapses. There are usually some rules about the timeline and the notices that the insurance company must provide to the customer before their pending lapse in coverage.

What often happens is people who lose their jobs stop paying and the ones that get into an accident get caught up on their payments so they can fix their car. Fraud also tends to spike during economic declines. Non-standard auto insurers have to be very good about ensuring that they don’t cover you for one day longer than they are required, because when a large portion of your customers only decides to pay you if they have an accident, your loss rates spike.

If you’ve ever followed auto insurers you may have heard that in good times standard auto insurers (think GEICO & State Farm) will dip down into the non-standard market only to pullback when loss ratios spike. A lot of this happens naturally as credit scores tend to inflate during economic expansions. In any case, how well Metromile is managing their non-standard underwriting is an open question. You might be thinking…well we just went through a massive unemployment spike and loss ratios have actually improved, but remember that this coincided with a very steep decline in driving and was coupled with a very large increase in unemployment insurance. I wouldn’t say that their underwriting has been fully tested so we’ll just have to wait and see.

Loss Ratio Marketing

Let’s say your job was to design a presentation to make your loss ratios look like they were moving in the right direction - someone has this job. How would you do it? First off, you would start your graph in 2016 to show a clear trend of lower loss rates, despite the fact that your business was merely a rounding error in that year (just $1.6mm in premiums earned). You would then fail to explain that the first half of this year cannot remotely be relied upon as an indication of what the future holds given the fact that everyone was home doing nothing.

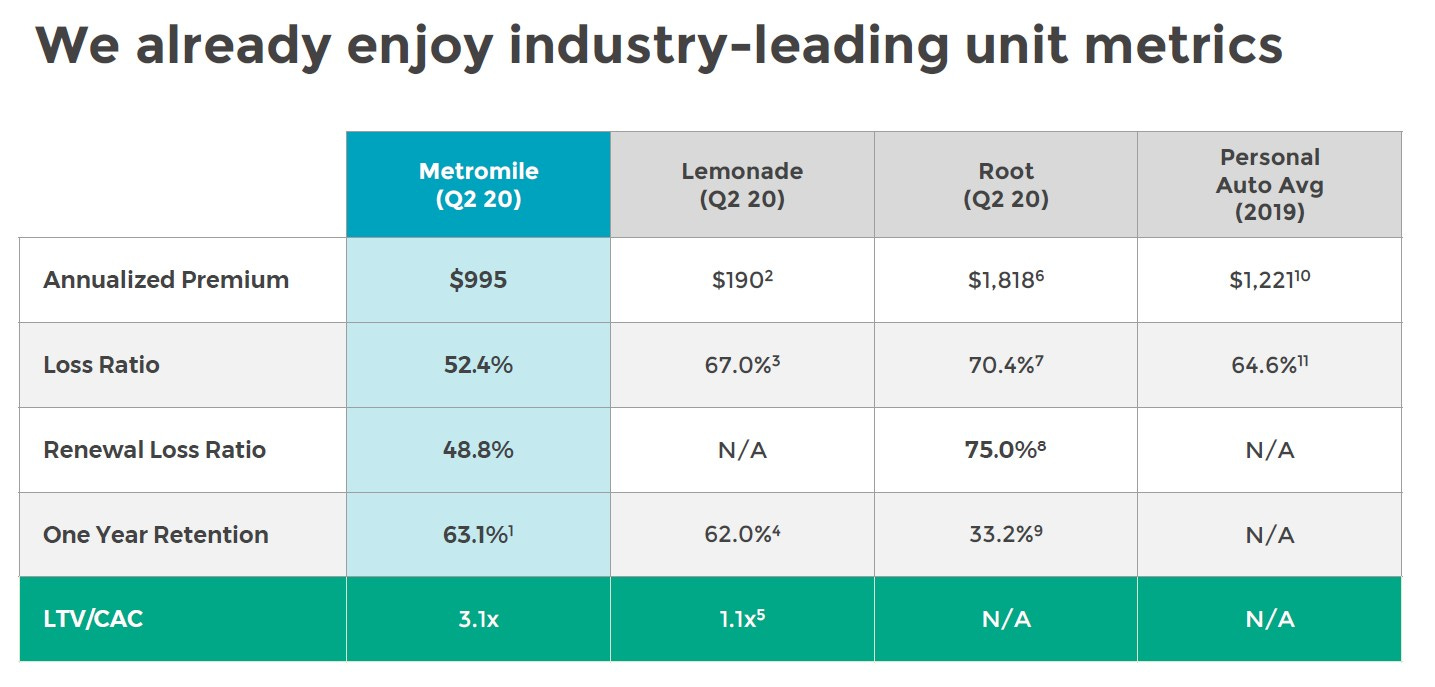

You would then compare yourself to one of the weaker competitors ($ROOT) whose premiums did not cover the companies losses and LAE in 2019, but was similarly helped by Covid. For those who are not well versed in insurance, loss adjustment expenses (LAE) are expenses for investigating & settling claims and are separate from the loss ratios reported above and below. Then, for some reason, you would compare yourself to a company that provides mostly rental insurance ( ¯\_(ツ)_/¯ ). And finally you would compare your loss ratio during a pandemic against the industry’s loss ratio while everyone was still driving. And voila…

It is my opinion that Metromile is using an unsustainable loss ratio to justify its growth plans. In 2019 Metromile’s loss ratio was 73.0% (vs. the 52.4% reported in Q2 above) and this compares to the industry loss ratio of 64.6%, presented above.

According to Metromile there is a linear relationship between miles driven and expected losses, but Metromile charges a fixed fee (to cover fixed costs) along with a per-mile fee (presumably to cover losses). If miles driven falls a lot the loss ratio naturally falls. If Metromile wants to prove that their loss ratio fell because of something other than Covid (like better underwriting) all they have to do is show us a loss ratio excluding the premiums related to the fixed-fee component. They have not.

Some Parting Thoughts About the Environment

We are in one of those strange periods where dreams move stocks and hindsight bias is all around us. Is this what the the tech bubble felt like? Yes, a little, but it ran for a lot longer than anyone expected and by the end, examples of stocks that required a lot of imagination where everywhere. Remember that in these periods the smartest investors can look like the dumbest and vice versa. Beware soothsayers and false prophets pitching SPACs. Whether this SPAC craze has a lot further to go I have no idea so best of luck and happy hunting…

hehe. this has aged like a fine claret.

Found this two years later and it is still incredibly thoughtful. Please write more.